Navigating the Trillion-Dollar Tide: What the US Debt News in 2026 Means for Your Finances

Educational Notice: This article is for educational and informational purposes only and is not financial, legal, or tax advice. Debt Planner is not a licensed financial advisor. Consider consulting a qualified professional before making financial decisions.

By Debt Planner Team, Content Team

The US national debt in 2026 is not Washington's problem. It is yours. Most personal finance advice treats government borrowing as background noise, something economists argue about while you focus on your budget spreadsheet and debt snowball plan. That separation is a costly illusion. Every trillion dollars the federal government adds to its balance sheet puts measurable upward pressure on the interest rates attached to your mortgage, your credit cards, and your student loans. Ignoring the macro picture while trying to fix your micro finances is like bailing out a boat without checking for the hole.

The US National Debt 2026 picture is stark. The federal debt has surpassed $36 trillion, with annual deficits running well above $1.5 trillion. Mortgage rates remain elevated above 6.5% as Treasury yields stay high to attract buyers for that debt. Credit card interest rates are averaging over 21%, a direct downstream effect of the Federal Reserve's prolonged high-rate posture. U.S. credit card debt has crossed $1 trillion, according to research cited by Northwestern's Kellogg School of Management. These four facts, taken together, mean the cost of carrying any debt in 2026 is punishing in ways that would have seemed extreme a decade ago.

The Federal Deficit Impact on Your Interest Rates

The connection between government borrowing and your personal borrowing costs is not abstract. When the federal government runs a deficit, it must sell Treasury bonds to finance the gap. To attract enough buyers for an ever-growing pile of bonds, yields must rise. Those yields are the benchmark against which banks price mortgages, auto loans, and credit cards. The Federal Reserve's policy rate is one lever; Treasury market dynamics are another, and in 2026 both levers are working against borrowers.

For homeowners watching mortgage rate trends, this matters immediately. A 30-year fixed mortgage at 7% on a $400,000 loan costs roughly $2,660 per month in principal and interest. The same loan at 4% — the rate environment of 2020. Cost about $1,910. That $750 monthly difference is the federal deficit impact landing directly in your household budget. It is not a rounding error.

Credit card rates track the Fed funds rate with a markup, and that markup has widened as banks price in default risk during a high-rate environment. Understanding exactly how minimum payments are structured under these conditions is worth your time. The mechanics of credit card minimum payment calculations reveal how slowly balances shrink when rates exceed 20%, which is now the norm rather than the exception.

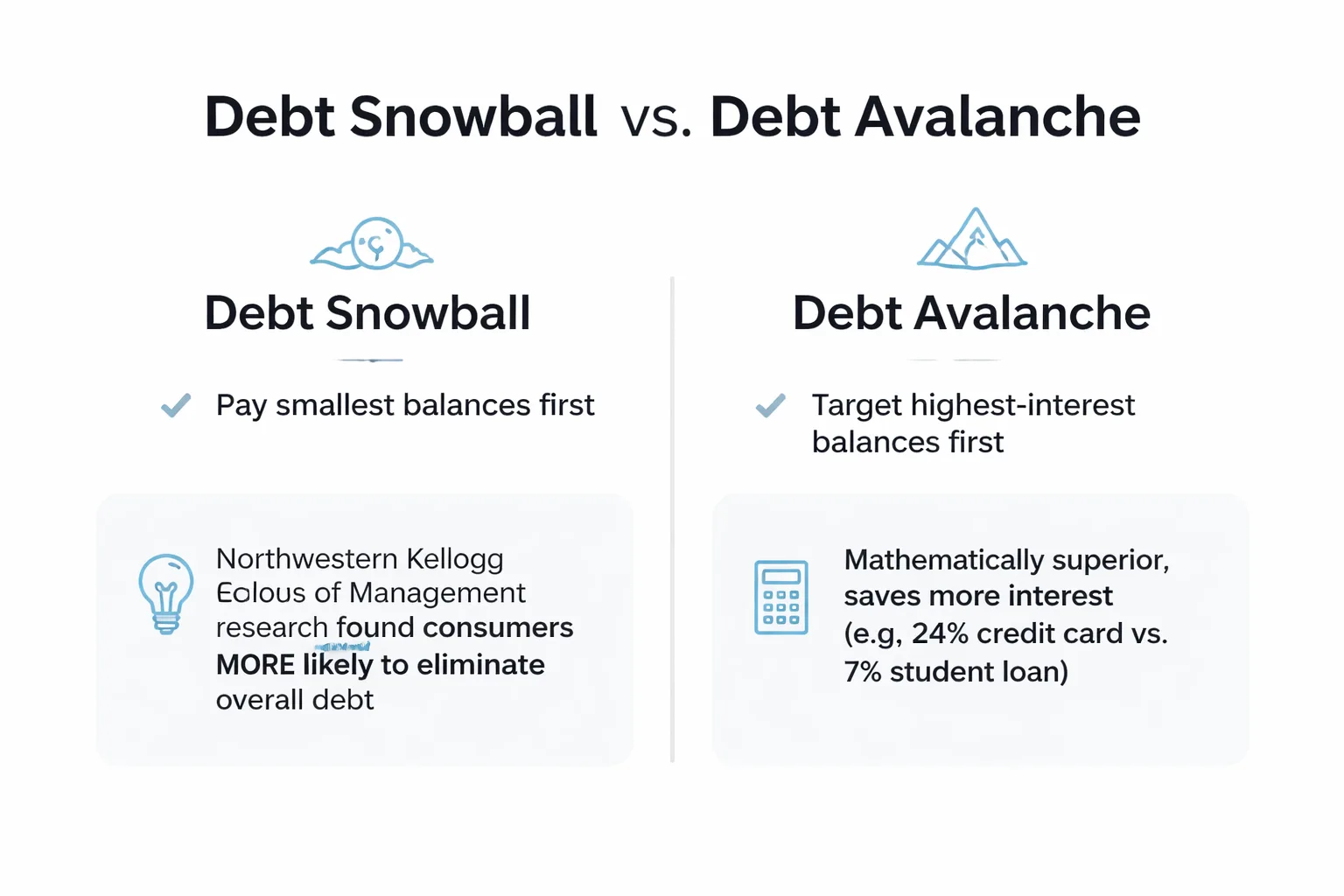

Debt Snowball vs. Avalanche: Which Actually Works?

Given that every debt on your balance sheet is now more expensive than it was two years ago, the question of repayment strategy is not academic. Two methods dominate the conversation: the debt snowball (paying smallest balances first) and the debt avalanche (targeting highest-interest balances first).

The avalanche is mathematically superior. Paying off a 24% credit card before a 7% student loan saves real money in interest. That is not debatable.

But math and behavior are different things. Research from Northwestern's Kellogg School of Management found that consumers who used the snowball approach — paying smallest balances first. Were actually more likely to eliminate their overall debt than those who optimized purely for interest rates. The mechanism is psychological: clearing a balance entirely, even a small one, creates a sense of momentum that keeps people in the game. "Small victories" compound into sustained behavior change. For a problem that is fundamentally about sticking with a plan over years, not months, that finding matters.

The honest answer is that the best strategy is the one you will actually execute. A side-by-side comparison of debt snowball vs. debt avalanche shows the real interest cost difference for your specific balances. And for many people carrying multiple debts, the gap is smaller than they expect. If the avalanche feels overwhelming, the snowball's psychological wins may keep you on track long enough to outperform the "optimal" approach you abandoned in month three.

For a more granular look at how these methods compare against each other and a third hybrid option, a debt snowball vs. avalanche vs. proportional calculator comparison lets you run your actual numbers rather than rely on generalizations.

Student Loan Repayment Strategy in a High-Rate World

Student loan repayment is where the macro environment gets genuinely complicated. Federal student loan interest rates for 2026 are set annually and have been climbing alongside Treasury yields. For graduate borrowers, rates on PLUS loans have exceeded 8% in recent cycles.

At those levels, the conventional advice to "just use income-driven repayment" deserves scrutiny. University of Colorado Boulder researchers developed a mathematical model finding that the optimal student loan repayment strategy is not universal. It depends on two key variables: how much you borrowed and what your income level is. Their model suggests that a mixture of repayment strategies may be optimal depending on individual circumstances, rather than a single rigid approach. A high earner with a modest loan balance is better served by aggressive payoff before interest compounds. A lower earner with a large balance may genuinely benefit from income-based repayment, particularly if they work in a qualifying public service role.

The practitioner takeaway: stop treating student loan repayment as a binary choice between "pay it off fast" and "stretch it out." The CU Boulder research implies that the right answer is situational, and that borrowers who dogmatically follow one path without modeling their specific numbers are likely leaving money on the table. The Consumer Financial Protection Bureau's student debt repayment guidance offers a structured framework for evaluating which repayment plan fits your income and loan type.

How to Read Your Bank Statements for Debt Reduction

Bank statement analysis is the unglamorous foundation of every debt reduction strategy. Before choosing snowball or avalanche, before refinancing, before anything else, you need to know where your money is actually going. Most people are surprised by what they find.

The process is straightforward. Pull three months of statements from every account. Categorize every transaction into four buckets: fixed obligations (rent, loan minimums, insurance), variable necessities (groceries, utilities, fuel), discretionary spending (restaurants, subscriptions, entertainment), and savings or debt overpayment. Total each bucket. The ratio between discretionary spending and debt overpayment is the number that matters most. If you're spending $400 a month on subscriptions and streaming services but only putting $50 extra toward your highest-interest card, that ratio tells you exactly where the leverage is.

Three months of data smooths out one-off expenses and reveals patterns that a single month hides. A quarterly gym membership that hits in January looks like a one-time charge until you see it again in April. Subscription creep. The slow accumulation of $9.99 and $14.99 monthly charges. Is almost universally underestimated until the statements are laid flat. One recurring finding across financial planning practice: people consistently underestimate their discretionary spending by 20-30% when asked to estimate from memory versus when they count from statements.

Once you've identified the gap between what you spend and what you could redirect to debt, the question becomes sequencing. That's where a structured debt payoff plan turns raw bank data into an actionable timeline.

Credit Card Debt: The Most Urgent Problem in 2026

Credit card debt is the financial emergency hiding in plain sight. At an average rate above 21%, a $5,000 balance costs over $1,000 per year in interest alone if you're making minimum payments. Stretch that out over five years of minimum payments and you've paid back the original $5,000 plus roughly $4,000 in interest, depending on your card's rate and minimum payment formula.

The trillion-dollar aggregate balance cited by Kellogg researchers is a population-level number. At the individual level, the math is more personal and more urgent. Every month you carry a balance at 21%+ is a month where inflation impact on debt is working against you in a compounding way. The federal deficit environment has kept rates high; there is no credible near-term forecast for credit card rates returning to the 15% range that was common before 2022.

The contrarian take that most financial content gets wrong: debt consolidation is not a strategy. It is a tool. Consolidating five credit cards into one personal loan at 12% saves real money in interest. But only if you stop using the cards you just zeroed out. The mechanics of debt consolidation are well-documented, but the behavioral discipline required to make it work is what separates people who consolidate and get ahead from those who consolidate and end up with both the personal loan and new card balances eighteen months later.

Mortgage Acceleration in a Persistent High-Rate Environment

For homeowners who bought or refinanced at low rates between 2020 and 2022, the calculus on mortgage acceleration is different from what it was a generation ago. A 3% mortgage in a world where Treasury bills yield 4.5% means the math actually favors investing surplus cash rather than prepaying principal. The opportunity cost is real.

For anyone who bought at current rates. Above 6.5% — the math flips. Prepaying a 7% mortgage is a guaranteed 7% return, risk-free. No investment vehicle offers that with certainty. Making one extra mortgage payment per year (by dividing your monthly payment by 12 and adding that amount to each monthly payment) typically shaves 4-6 years off a 30-year loan and saves tens of thousands in interest. On a $400,000 loan at 7%, that strategy saves roughly $80,000-$90,000 over the life of the loan.

The tension between emergency fund maintenance and mortgage acceleration is real and worth thinking through carefully. The emergency fund vs. debt payoff tradeoff has a clear answer for most people: maintain three to six months of expenses in liquid savings before directing surplus cash to mortgage prepayment. Prepaying your mortgage while carrying no emergency fund means a job loss or medical bill forces you into high-interest debt to cover expenses. Erasing the benefit of the prepayment entirely.

Why the Psychology of Debt Freedom Matters More Than the Math

The research on debt and mental health is unambiguous. A study published in Social Science & Medicine found that household financial debt has measurable negative impacts on both mental and physical health. A separate study published in PNAS found that reducing debt improves psychological functioning and changes decision-making patterns. Meaning that getting out of debt doesn't just feel better, it literally changes how people think and plan.

This is not a soft finding. It has hard practical implications for debt reduction strategies. People under financial stress make worse financial decisions. They're more likely to take payday loans, miss payment deadlines, and avoid opening statements. The stress of debt impairs the exact cognitive functions needed to manage debt well. Breaking that cycle requires early wins, which is exactly why the Kellogg snowball research matters: the psychological benefit of eliminating one balance entirely, even a small one, can restore enough cognitive bandwidth to make better decisions on the larger balances.

Budgeting for debt elimination works best when it accounts for this dynamic. A plan that is mathematically optimal but psychologically brutal. Requiring years of austerity before any visible progress. Has a high dropout rate. A plan that builds in small milestones and visible wins, even at a slight interest cost, is more likely to reach completion.

AI Tools and the Future of Personal Finance Debt Strategies

AI-powered personal finance tools have moved from novelty to genuinely useful in 2026. The most practical applications for debt management are: automated transaction categorization (which replaces the manual bank statement analysis described above), scenario modeling (running snowball vs. avalanche projections across your actual balances in seconds), and behavioral nudges (alerts when spending in a category threatens your debt payoff timeline).

Free tools like Free Debt Planner combine a debt payoff calculator with spending analysis, letting users see exactly how redirecting $200 per month from discretionary spending changes their debt-free date. The value is not the calculation itself. Anyone can do the arithmetic. The value is the visibility. Seeing a concrete date, watching it move forward as you add extra payments, creates the same psychological momentum the Kellogg snowball research identified. The tool makes the abstract concrete.

The broader point about AI in personal finance: the technology is most useful when it removes friction from decisions you already know you should make. It does not replace the discipline. It lowers the cognitive cost of exercising it.

Frequently Asked Questions

Does the US national debt directly affect my credit card interest rate?

Yes, indirectly but measurably. When the federal government borrows heavily, it competes with other borrowers for available capital, pushing up the yields on Treasury bonds. The Federal Reserve's benchmark rate, which banks use to price consumer credit, responds to these dynamics. Credit card rates in 2026 exceeding 21% on average reflect both Fed policy decisions and the broader pressure of sustained federal deficit spending on credit markets.

Should I prioritize debt payoff or investing right now given high interest rates?

The answer depends on your rates. Any debt above 7% almost certainly deserves priority over stock market investing, because the guaranteed return from eliminating that debt exceeds what most diversified portfolios can reliably deliver. Below 5% — particularly older fixed-rate mortgages. The math may favor investing. The emergency fund vs. debt payoff balance should be resolved first: maintain liquid reserves before aggressively paying down any debt.

How much does carrying credit card debt actually cost at 2026 rates?

At a 21% APR, a $10,000 balance costs approximately $2,100 per year in interest if you make only minimum payments. Over five years of minimum payments, you would pay back the original $10,000 plus roughly $8,000-$9,000 in interest depending on your card's minimum payment formula. The mechanics of minimum payment calculations explain exactly why balances shrink so slowly under this structure.

Is debt consolidation a good idea in the current rate environment?

For credit card debt above 20%, consolidating into a personal loan at 10-14% saves meaningful money. But only if you don't accumulate new card balances afterward. Consolidation reduces your interest burden; it does not address the spending patterns that created the debt. Treat it as a rate arbitrage tool with strict behavioral guardrails, not a clean slate.

What is the fastest way to become debt-free given current economic conditions?

The fastest path combines three moves: a thorough bank statement audit to identify redirectable cash, a structured payoff sequence (snowball or avalanche based on your psychology and balance profile), and elimination of high-rate debt before any discretionary investing. Research consistently shows that people who create a written payoff plan with specific monthly targets eliminate debt faster than those who "try to pay more when possible." Specificity beats intention every time.

Published with Meev

Important: Debt Planner is an educational tool only. We are not licensed financial advisors, credit counselors, or debt management professionals. All calculations are for educational purposes. Please consult qualified financial professionals before making significant financial decisions.

© 2025 Debt Planner. All rights reserved.