How to Read Your Bank Statements and Cut Debt Faster

Educational Notice: This article is for educational and informational purposes only and is not financial, legal, or tax advice. Debt Planner is not a licensed financial advisor. Consider consulting a qualified professional before making financial decisions.

By Debt Planner Team, Content Team

Key Takeaways

- Bank statement analysis costs nothing, requires no app, and takes under an hour yet most people skip it, costing them months or years of extra debt repayment time.

- The CFPB's Making Ends Meet Survey found 40% of consumers had difficulty paying a bill or expense in the year before the pandemic.

- PNAS research shows reducing debt directly improves psychological functioning and rewires decision-making patterns around money.

- Credit card debt fell sharply in the first months of the pandemic—even among financially vulnerable consumers—when external pressure forced spending awareness.

Bank statements as we know them trace back to the mid-19th century, when American commercial banks began mailing paper ledgers to depositors so they could reconcile their accounts by hand. For over 150 years, that monthly document served one purpose: verification. Nobody told you it could be a weapon against your own debt. It wasn't until behavioral economists in the early 2000s began studying spending transparency that researchers confirmed what savers had quietly discovered. Systematically reviewing your transactions changes how you spend money, and how fast you pay debt off.

Bank statement analysis is the single most underused debt reduction strategy available to anyone with a checking account. It costs nothing, requires no app, and takes under an hour. Yet most people scan their statement once a month, confirm nothing looks fraudulent, and close the tab. That habit is costing them months. Sometimes years. Of debt repayment time.

Bank statement analysis exposes the exact dollar amounts draining your debt payoff capacity each month. Research published in PNAS found that reducing debt directly improves psychological functioning and changes decision-making patterns in low-income populations. Meaning the act of paying down debt isn't just financial, it rewires how you think about money going forward. The CFPB's Making Ends Meet Survey found that 40% of consumers had difficulty paying a bill or expense in the year before the COVID-19 pandemic. That's not a fringe problem. A separate CFPB issue brief documented that credit card debt fell sharply in the first months of the pandemic — even for financially vulnerable consumers. Suggesting that when external pressure forces spending awareness, people pay down debt faster. The lesson: awareness works. The question is how to manufacture it deliberately, without a pandemic forcing your hand.

Why Your Bank Statement Is Your Best Debt-Reduction Tool

Most people treat their bank statement like a receipt. It's not. It's a diagnostic report. A month-by-month record of every financial decision, impulse, and habit playing out in real life. The gap between what people think they spend and what they actually spend is routinely 20-30%, according to budgeting research. That gap is where debt repayment dollars go to die.

The statement doesn't lie. It doesn't round up your dining expenses or forget the three streaming services you haven't used since January. It captures everything, which is exactly why most people don't look at it closely. Looking closely means confronting uncomfortable truths about spending patterns that feel minor in isolation but compound into serious debt drag over time.

Here's the core insight: every dollar you spend on something non-essential is a dollar that isn't reducing your highest-interest debt. At a 22% APR (the current average for credit cards in the U.S.), a $50 monthly subscription you don't use isn't costing you $50. It's costing you $50 plus the interest that $50 would have eliminated if it had gone toward your balance. Over a year, that single subscription costs you $600 in principal plus the compounding interest on that $600. Bank statement analysis makes those invisible costs visible.

For anyone working through debt reduction strategies, the statement is ground zero. Before you choose between the debt snowball or debt avalanche, before you consider debt consolidation, you need to know exactly how much money is actually available to redirect toward debt. The statement tells you.

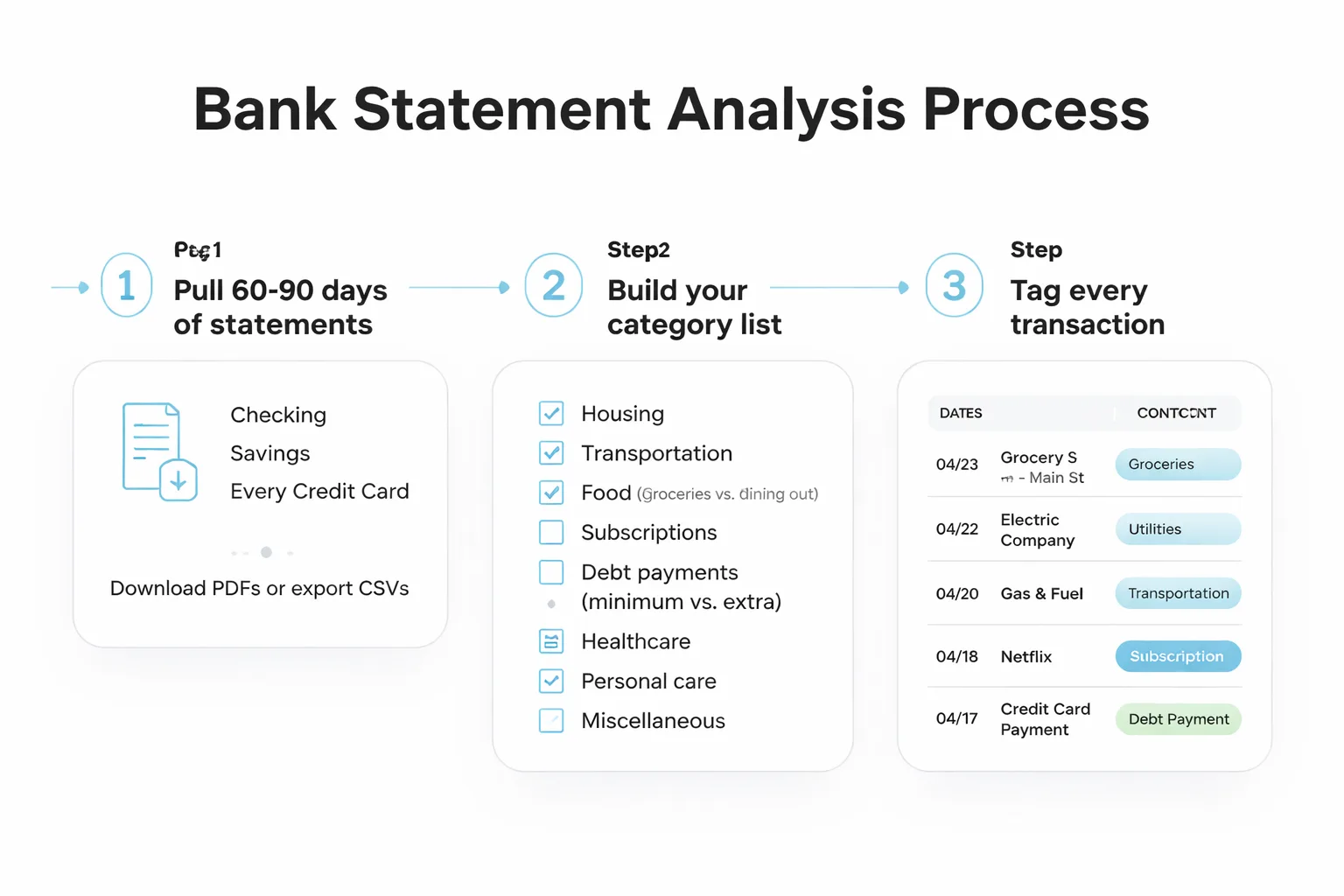

Step-by-Step: How to Categorize Your Transactions

The process is straightforward, but the details matter. Here's the method that produces the clearest picture of where your money is going.

Step 1: Pull 60-90 days of statements. One month is too noisy. It might include a one-time expense or miss a quarterly charge. Three months reveals patterns. Download PDFs or export CSVs from your bank's online portal for every account: checking, savings, and every credit card.

Step 2: Build your category list. Don't use generic categories. Build ones that match your actual life. A workable set includes: housing (rent/mortgage, utilities, insurance), transportation (car payment, fuel, parking, rideshare), food (groceries vs. dining out. Keep these separate), subscriptions (streaming, software, memberships), debt payments (minimum payments vs. extra payments. This distinction matters), healthcare, personal care, and miscellaneous. The more granular your categories, the more useful the analysis.

Step 3: Tag every transaction. This is the tedious part, but it's also where the insights live. Go line by line. When you hit an unfamiliar merchant name, look it up. Many subscription charges appear under obscure parent company names. A charge labeled "VZWRLSS" is Verizon Wireless. "AMZN MKTP" is Amazon. Don't skip anything.

Step 4: Calculate category totals and percentages. Once everything is tagged, total each category and divide by your take-home income. The percentages are more revealing than the dollar amounts. Spending $400 on dining means something different if you earn $3,000 a month versus $8,000 a month. The ratio tells you where your priorities are actually landing, not where you think they are.

Step 5: Compare against your debt payment line. Look at what percentage of income is going toward debt payments. Then look at what percentage is going toward discretionary categories. The ratio between those two numbers is your debt payoff velocity. If discretionary spending is three times your debt payments, you have a structural problem that no debt repayment strategy can fully fix without first addressing the spending side.

The 5 Spending Patterns That Quietly Sabotage Debt Payoff

Bank statement analysis consistently surfaces the same culprits across different income levels and debt loads. These five patterns appear in virtually every statement review.

1. Forgotten subscriptions. The average American household carries more active subscriptions than they can name from memory. At $10-$20 per service, three forgotten subscriptions cost $360-$720 per year. That's not a rounding error. At 22% APR, $720 redirected to credit card debt eliminates the principal AND prevents roughly $158 in annual interest charges. The combined impact is nearly $900 in real financial value from canceling three services you weren't using.

2. Minimum-only credit card payments. This one is structural, not behavioral. But it shows up on statements as a pattern that most people never question. Understanding how minimum payment calculations actually work is essential here, because banks design minimums to maximize the interest you pay over time. A $5,000 balance at 22% APR with minimum payments only takes over 17 years to eliminate and costs more than $6,000 in interest. The minimum payment line on your statement is the single most expensive line item most people never scrutinize.

3. Frequent small purchases adding up to large monthly totals. Coffee shops, convenience stores, fast-casual restaurants. Individually these feel trivial. Collectively they often represent the second or third largest discretionary category on a statement. A $6 daily coffee habit runs $180 a month, $2,160 a year. That's not a judgment about coffee. That's math. If $2,160 went toward a credit card balance instead, it would eliminate the principal and cut months off the repayment timeline.

4. Duplicate or overlapping services. Two cloud storage subscriptions. A gym membership plus a fitness app. Cable TV plus three streaming services that cover the same content. Statement analysis surfaces these overlaps because you see every charge in sequence. Most people don't realize they're paying for the same category twice until they see it written out.

5. Irregular large expenses treated as surprises. Car registration. Annual insurance premiums. Holiday spending. These aren't surprises. They happen every year. But because they don't appear monthly, people treat them as one-time disruptions and often put them on credit cards. Statement analysis over 90 days will catch at least one or two of these, which is enough to build a sinking fund strategy so they never hit a credit card again.

Curious how much your spending leaks are really costing your debt payoff timeline?

Analyze My Spending Free →

How Does Bank Statement Analysis Connect to Debt Strategy?

Knowing where your money goes is only useful if it changes what you do next. The connection between bank statement analysis and debt payoff strategy is direct: the leaks you identify become the fuel for acceleration.

Here's a simple reallocation formula. After completing your categorization, identify your "recoverable" dollars. Subscriptions you'll cancel, dining you'll reduce, overlapping services you'll consolidate. Be conservative. If you spend $400 on dining and think you can cut it to $200, use $150 as your estimate. Behavioral change is harder than it looks on a spreadsheet.

Add up your conservative recoverable total. Even $100-$150 per month is significant. At $150 extra per month applied to a $5,000 credit card balance at 22% APR, the payoff timeline drops from 17+ years (minimum payments only) to under 3 years. The interest savings exceed $5,500. That's the compounding math of acceleration: small consistent additions don't just reduce the balance, they collapse the timeline.

Once you know how much you can redirect, you need a strategy for where to send it. The two primary frameworks are the debt snowball and debt avalanche. The avalanche method (paying highest-interest debt first) is mathematically optimal and will save the most money in total interest. The snowball method (paying smallest balance first) is psychologically powerful. Research from the Kellogg School found that consumers who paid off smallest balances first were more likely to eliminate their overall debt. Even though the avalanche approach would have saved them more money. The right choice depends on whether you need mathematical efficiency or motivational momentum.

For anyone carrying multiple debt types. Credit cards, student loans, a mortgage. The comparison of all three payoff methods is worth running before committing to a single approach. The proportional method, which splits extra payments across all debts by balance size, sometimes outperforms both snowball and avalanche in specific debt configurations.

The psychology matters more than most financial advice acknowledges. The PNAS study mentioned earlier found that reducing debt improves psychological functioning and changes decision-making. Meaning early wins from a snowball approach don't just feel good, they may actually improve the quality of your subsequent financial decisions. That's a meaningful finding for anyone who has started a debt payoff plan and abandoned it within three months.

When Should You Revisit Your Budget Allocation?

Budgeting for debt isn't a one-time exercise. Spending patterns shift, income changes, and the debts themselves evolve as balances drop. A bank statement analysis done once produces a snapshot. Done quarterly, it produces a system.

The trigger points for a full re-analysis are: any income change (up or down), paying off a debt entirely (those freed-up payment dollars need to be redirected immediately or they disappear into lifestyle inflation), a major new expense, and any time you feel like your debt payoff has stalled despite consistent effort. Stalling is almost always a spending pattern problem, not a strategy problem.

For anyone also managing an emergency fund alongside debt payoff, the spending analysis is equally important. The balance between emergency fund and debt payoff is a legitimate strategic question, and the answer depends partly on how much cash flow your statement analysis reveals you actually have available. You can't make that decision in the abstract.

One more consideration: credit card debt reduction has a direct downstream effect on your credit score. As balances drop and utilization falls, scores typically rise. What happens to your credit score when you pay off debt follows a predictable timeline. Understanding it helps you set realistic expectations and stay motivated through the process.

Let AI Do the Heavy Lifting: Automated Spending Analysis

The manual process described above works. It also takes 2-3 hours the first time, which is why most people do it once and don't repeat it. That's the gap that automated bank statement analysis tools are designed to close.

Free Debt Planner's transaction categorization feature connects to your accounts and does the tagging automatically. Grouping transactions into categories, calculating percentages, and surfacing the patterns that typically take hours to find manually. The platform supports credit cards, student loans, and mortgages, so the analysis isn't siloed to one debt type. It shows the full picture: what you owe, what you're spending, and where the reallocatable dollars are hiding.

The practical difference between manual and automated analysis isn't just time. It's consistency. A tool that categorizes your transactions every month produces 12 data points per year. Manual analysis, realistically, produces two or three. The compounding value of monthly visibility is significant. You catch spending drift before it becomes a structural problem, and you can see immediately whether your debt payoff is accelerating or stalling.

For anyone who wants to run the numbers before committing to a full setup, a debt payoff calculator is the fastest way to see what a $100 or $200 monthly increase in payments actually does to your payoff timeline. The math is often more motivating than any amount of abstract advice.

The CFPB data showed something counterintuitive: even financially vulnerable consumers reduced credit card debt during the pandemic, when external circumstances forced a sudden shift in spending behavior. The mechanism was awareness and constraint. Automated bank statement analysis replicates that awareness without requiring a crisis to trigger it. That's the real value proposition: not novelty, but consistency.

Frequently Asked Questions

How often should I do a bank statement analysis for debt reduction?

Quarterly is the minimum for meaningful pattern detection, but monthly is better. Spending behavior drifts gradually. A monthly review catches new subscriptions, creeping dining costs, or missed debt payment opportunities before they compound. If you're using an automated tool, weekly summaries are practical and take under five minutes to review.

What's the most important thing to look for in a bank statement when trying to pay off debt?

The ratio between your debt payments and your discretionary spending. If discretionary categories (dining, entertainment, subscriptions, shopping) collectively exceed your total debt payments, you have more room to accelerate payoff than your current plan reflects. That gap is the first place to look for reallocation opportunities.

Does analyzing my spending actually speed up debt payoff, or is it just awareness?

Both. And the research suggests they're connected. The 2019 PNAS study found that reducing debt improves decision-making, and behavioral economists have documented that spending transparency changes spending behavior. Awareness isn't passive. When you see a number attached to a habit, you make different choices about that habit.

Should I analyze statements for all accounts, or just checking?

All accounts. Credit card statements are especially important because they capture spending that doesn't appear in your checking account until the payment clears. Analyzing only your checking account misses the full picture of where money is going and understates your true monthly spend in most categories.

What if my income is irregular? Does bank statement analysis still work?

Yes, but use percentage-based targets rather than fixed dollar amounts. If income varies month to month, a rule like "20% of whatever I earn goes to debt payments" is more sustainable than a fixed $400 target. The statement analysis still surfaces the spending patterns. The reallocation formula just needs to flex with income rather than stay fixed.

How does bank statement analysis relate to choosing between debt snowball and avalanche?

Directly. The analysis tells you how much extra money you can realistically redirect to debt each month. That number affects which strategy is optimal. If you can free up $300+ per month, the avalanche method's interest savings are substantial. If you can only free up $50-$75, the motivational boost from the snowball method may matter more for long-term follow-through. Run the numbers on both before deciding.

Let Free Debt Planner categorize your transactions automatically and show you exactly where your debt payoff dollars are going — no spreadsheet required.

Analyze My Spending Free

Important: Debt Planner is an educational tool only. We are not licensed financial advisors, credit counselors, or debt management professionals. All calculations are for educational purposes. Please consult qualified financial professionals before making significant financial decisions.

© 2025 Debt Planner. All rights reserved.