How to Choose a Debt Payoff Method in 5 Clear Steps

Educational Notice: This article is for educational and informational purposes only and is not financial, legal, or tax advice. Debt Planner is not a licensed financial advisor. Consider consulting a qualified professional before making financial decisions.

By Debt Planner Team, Content Team

Key Takeaways

- The debt snowball (smallest balance first) builds momentum through quick wins, while the debt avalanche (highest rate first) minimizes total interest — with average credit card APRs at 24.26% versus 7.51% for private student loans, the rate spread often makes avalanche the cheaper choice.

- Picking the wrong method for your psychology — not lack of willpower — is the most common reason debt repayment stalls; honest self-assessment in Steps 3 and 4 is what makes the framework work.

- Automating every minimum payment and directing extra dollars to a single target debt removes willpower from the equation and makes the plan structurally resilient.

- The three most common post-commitment mistakes are switching methods too early, accumulating new debt during payoff, and treating early snowball wins as the finish line — each has a specific structural fix.

The debt payoff method you choose matters far less than personal finance influencers want you to believe. But choosing none at all will quietly wreck you. The debt snowball gets dismissed as mathematically inferior, while the avalanche gets called too slow for real people to stick with. Both criticisms miss the point entirely. The best debt payoff method is the one calibrated to your actual balances, income patterns, and emotional relationship with money. Stop debating which strategy is objectively superior and start using this five-step process to find out which one is superior for you.

Why Your Payoff Method Matters More Than Your Motivation

Most people who stall on debt repayment blame themselves. They call it a willpower problem, a discipline problem, a personality problem. The data tells a different story. The CFPB notes that the snowball method lets borrowers "see progress quickly" but warns it "may end up paying more in the long run," while Fidelity's analysis states the avalanche "generally saves you the most on interest payments, particularly if you have loans with a wide range of interest rates." Neither institution frames this as a willpower issue. Both frame it as a strategy-fit issue.

The problem isn't motivation. The problem is mismatch. Someone with eight small debts who commits to the debt avalanche is going to spend six months grinding on a high-rate balance with no visible finish line. Someone with two large debts at similar rates who commits to the debt snowball is leaving real money on the table for zero psychological benefit. Picking the wrong structure for your specific debt profile is the most common reason people quit, not character weakness.

This five-step framework solves the mismatch problem. It forces you to look at your actual numbers before making a strategy decision, then gives you a structured way to match those numbers to your psychology. The goal isn't to sell you on one method. The goal is to make the right method obvious.

Step 1. 2: List Your Debts and Know Your Numbers

Before any strategy decision, the data has to be on the table. This sounds obvious. Almost nobody does it correctly.

Step 1 is a complete debt inventory. Pull every balance: credit cards, student loans, personal loans, car loans, medical debt, any mortgage. For each one, record four things: the current balance, the interest rate (APR), the minimum monthly payment, and the lender name. Don't estimate. Log into each account and pull the exact figures. A $200 difference in your estimated versus actual balance on a high-rate card can meaningfully change which method makes sense.

Step 2 is running the numbers through a debt payoff calculator before you choose anything. This step is where most people skip ahead and pay for it later. A calculator surfaces what gut instinct can't: the total interest cost under each method, the payoff timeline for each debt, and the order of operations that minimizes either time or cost. The spread between interest rates matters enormously here. According to Experian, the average credit card APR sits at 24.26%, while the average 10-year private student loan rate is 7.51%. That's a 16-point spread. If your debt mix looks anything like that national average, the avalanche method's mathematical advantage is not marginal. It's substantial. Paying off a $10,000 credit card balance at 24% before a $10,000 student loan at 7.5% isn't a close call on paper.

But here's what the calculator also shows you: the snowball method's payoff timeline for your smallest balances. If you have three debts under $800 that could be eliminated within 60 to 90 days, the behavioral calculus shifts. Eliminating those three payments simplifies your financial picture immediately and generates the kind of reinforcement that keeps people on plan. The 30-to-60-day quick win is a legitimate strategic consideration, not just emotional comfort. A debt that disappears in two months is worth treating differently than one that takes two years, even if the interest rate math slightly favors another order.

Once you have your inventory and your calculator output, you have something most people lack: actual information. Now the strategy decision becomes diagnostic instead of philosophical.

Step 3. 4: Match Your Psychology to the Right Strategy

Step 3 is honest self-assessment. Not the version where you tell yourself you're disciplined because you want to be. The version where you look at your history.

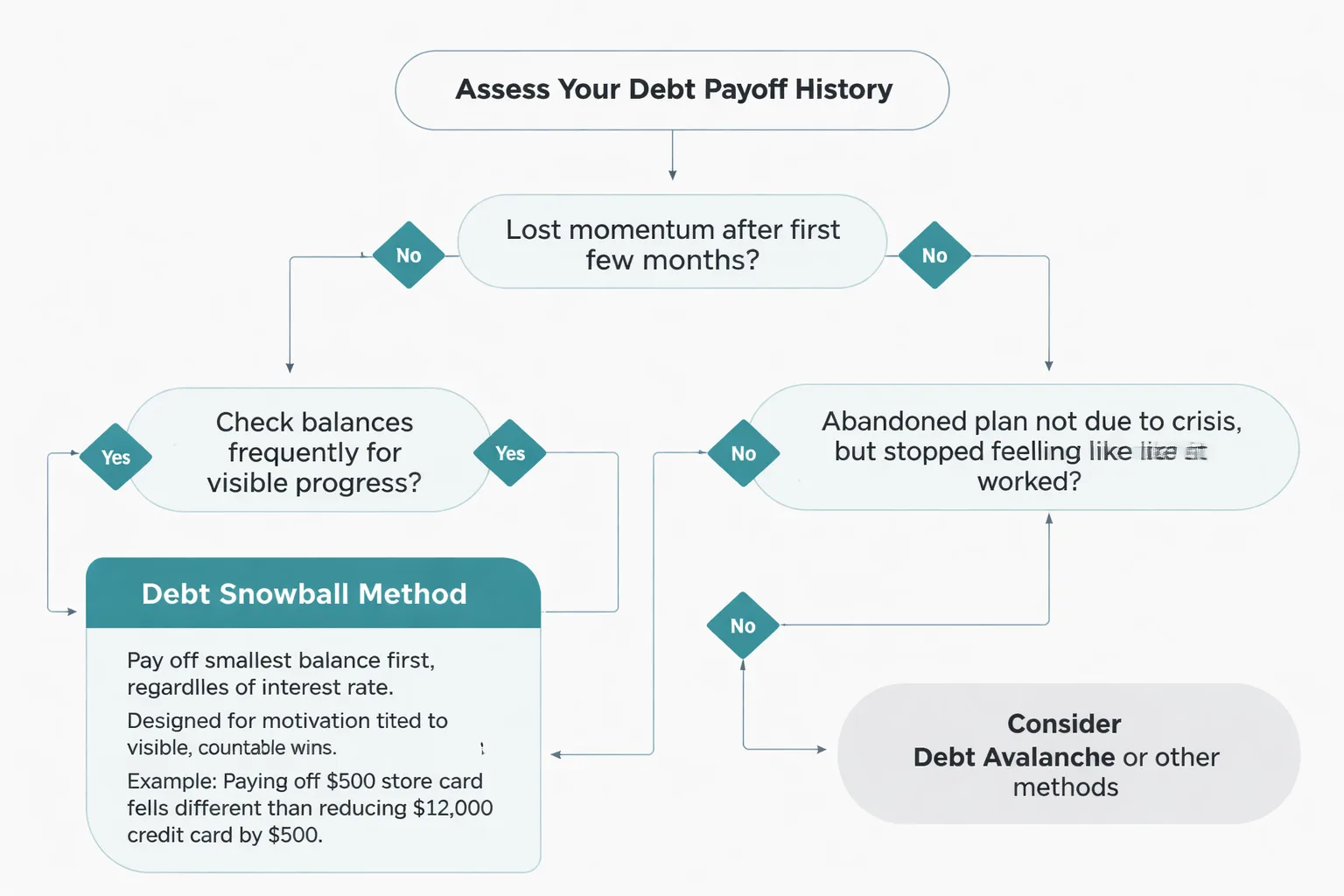

Ask these questions about your last debt payoff attempt (or your current one): Did you lose momentum after the first few months? Do you check your balances frequently looking for visible progress? Have you ever abandoned a financial plan not because of a crisis but because it stopped feeling like it was working? If yes to any of these, the debt snowball is almost certainly your method. The psychological architecture of the snowball. Smallest balance first, regardless of interest rate. Is specifically designed for people whose motivation is tied to visible, countable wins. Paying off a $500 store card feels different than reducing a $12,000 credit card balance by $500, even if the dollar amounts are identical. The account closure is the signal. The brain responds to it.

If, on the other hand, you've historically stayed the course on long-horizon plans, you track your net worth regularly, and the idea of paying more in total interest genuinely bothers you more than a slow start bothers you, the debt avalanche is your method. You're optimizing for the right thing: minimizing the total cost of your debt, not the emotional experience of paying it. As Fidelity puts it, "you'll save more on interest with the avalanche method, but using the snowball method can be emotionally satisfying" — and for some people, that satisfaction is the mechanism that makes the plan work at all.

Step 4 is where the hybrid case gets addressed honestly. The strict snowball-versus-avalanche framing breaks down for a specific debt profile: someone who has one or two very small balances (under $500, clearable in 30 to 60 days) alongside several larger high-rate debts. In that case, clearing the small balances first. Even under an otherwise avalanche approach. Is not a compromise. It's a rational behavioral strategy. The psychological reinforcement from eliminating those accounts early is immediate, and the interest cost difference on a $400 balance is negligible. After those quick wins, the avalanche logic takes over cleanly. This hybrid approach is worth considering before defaulting to a pure method in either direction.

For a deeper breakdown of how these methods compare across different debt profiles, the debt snowball vs. avalanche comparison runs through specific scenarios with numbers.

Not sure whether the debt snowball or avalanche fits your situation better?

Build Your Free Plan →

Step 5: Build Your Plan and Automate It

Deciding on a method is not the same as having a plan. A plan has a written order of operations, a specific dollar amount allocated above minimums each month, and a mechanism that removes the decision from your hands every payment cycle.

Start by writing the payoff order. Whether you've chosen snowball or avalanche, list your debts in the sequence you'll attack them. Debt 1 gets all extra payments. Debts 2 through N get minimum payments only. This is not complicated, but writing it down matters. Research on implementation intentions. The psychology of "if-then" planning. Consistently shows that people who write down the specific action they'll take follow through at higher rates than those who only decide in the abstract.

Next, set every minimum payment to autopay. Every single one. The goal is to make it structurally impossible to accidentally miss a minimum on a debt you're not actively targeting. A missed payment on a background debt can trigger a penalty APR, damage your credit score, and undo weeks of progress. Automation eliminates that risk entirely.

Then direct your extra payment. Whatever you've carved out above minimums. To the target debt. If that's a manual transfer, automate it too. The moment payment decisions require active willpower each month, the plan is fragile. Automation converts the plan from a recurring decision into a system.

For tracking, a free AI-powered tool like Free Debt Planner handles the math that spreadsheets make tedious: recalculating your payoff timeline as balances change, projecting total interest saved, and flagging when it's time to roll your payment to the next debt. This kind of real-time feedback is what keeps the plan legible month to month, especially during the middle phase of debt payoff when progress feels invisible. You can also use it to run a debt payoff calculator scenario before committing to a new approach.

One final structural note: the emergency fund question. Automating debt payments without any cash buffer is a plan that one car repair away from collapse. The emergency fund vs. debt payoff tradeoff is real, and the answer isn't all-or-nothing. A $1,000 starter emergency fund before accelerating debt payments is the standard threshold most financial planners recommend. It's not a large number, but it's enough to absorb most common financial shocks without forcing you to put new debt on a credit card and restart the cycle.

Common Mistakes to Avoid Once You've Chosen a Method

Choosing a method is the beginning, not the finish line. The most common failure modes happen after the decision, not before it.

Switching methods too early. The debt snowball's first payoff can take two to four months for someone with a $600 target balance. The avalanche's first payoff on a $8,000 high-rate card can take a year or more. Both timelines feel slow in month three. The mistake is interpreting "this feels slow" as "this method is wrong" and switching. Switching resets the psychological clock without changing the underlying math. If the method matched your profile in Step 3, the answer to feeling slow is almost never to switch. It's to revisit whether your monthly extra payment amount is realistic. The CFPB's guidance on reducing debt is explicit: consistency with one approach outperforms frequent strategy changes.

Ignoring new debt. The plan assumes a closed system: the debts you listed in Step 1 are the debts you're paying off. New credit card charges that aren't paid in full each month are a leak in that system. They don't just add balance. They can change the optimal payoff order and extend your timeline in ways the original plan didn't account for. The fix is a hard rule: during active debt payoff, credit cards get paid in full monthly or they don't get used. This isn't about punishment. It's about not running the bathtub with the drain open.

Skipping the overconfidence check. This one is counterintuitive. The debt snowball's early wins are genuinely motivating. And that motivation can tip into a "mission accomplished" mindset after the first two or three accounts close. The pattern shows up repeatedly in practitioner forums: someone eliminates $1,500 in small debts, feels financially free, relaxes spending discipline, and starts accumulating new balances before the larger debts are gone. The fix is explicit milestone-setting beyond the first few wins. Map out the full payoff sequence in Step 5 and mark the actual finish line, not just the early ones. The goal is debt freedom, not just a shorter debt list. For context on what that finish line looks like for your credit profile, the credit score impact of paying off all debt is worth understanding before you get there.

Frequently Asked Questions

Is the debt snowball or debt avalanche better for credit card debt specifically?

For credit card debt, the avalanche method typically produces lower total interest costs because average credit card APRs run at 24.26% — well above most other debt types. If your credit card balances are large and will take over a year to clear, the avalanche's interest savings are meaningful. If your credit card balances are small enough to eliminate within 60 to 90 days, the snowball's quick-win logic applies and the interest difference is minor. The minimum payment trap is also worth understanding. Minimum-only payments on high-rate cards extend timelines dramatically.

Can someone use a debt management plan instead of snowball or avalanche?

A debt management plan (DMP) through a nonprofit credit counselor like the NFCC is a different category of solution. DMPs consolidate multiple payments, often negotiate reduced interest rates with creditors, and provide structured repayment over three to five years. They're worth considering when interest rates are too high to make meaningful principal progress with snowball or avalanche alone. DMPs and the avalanche method aren't mutually exclusive. A DMP can lower the rates, and avalanche logic can determine which remaining balances to prioritize.

What if someone has both student loans and credit card debt?

Prioritize credit card debt first in almost every case. With average private student loan rates at 7.51% versus average credit card APRs above 24%, the interest rate spread makes credit cards the clear avalanche priority. Federal student loans also carry income-driven repayment options and potential forgiveness programs that credit cards don't, making them structurally lower-urgency for most borrowers.

How often should someone revisit their chosen method?

A monthly check-in is sufficient for most people. The check-in should cover three things: confirming autopayments processed correctly, updating balances in the tracking tool, and checking whether any new debt has entered the picture. A full strategy review. Reconsidering snowball versus avalanche. Is warranted only when a major life change occurs: significant income change, a new large debt, or a windfall that could accelerate the plan meaningfully.

What's the fastest way to pay off debt if neither method feels right?

Debt consolidation is worth evaluating when multiple high-rate balances make the payoff order feel unmanageable. Combining debts into a single lower-rate loan simplifies the structure and can reduce total interest. The debt consolidation overview covers when it makes sense and when it doesn't. Consolidation isn't always an improvement, particularly if the new loan extends the repayment term significantly.

Run your numbers through Free Debt Planner and get a personalized payoff order in minutes — no spreadsheet required.

Build Your Free Plan

Important: Debt Planner is an educational tool only. We are not licensed financial advisors, credit counselors, or debt management professionals. All calculations are for educational purposes. Please consult qualified financial professionals before making significant financial decisions.

© 2025 Debt Planner. All rights reserved.