Debt Snowball vs. Avalanche: Which Actually Wins in 2026?

Educational Notice: This article is for educational and informational purposes only and is not financial, legal, or tax advice. Debt Planner is not a licensed financial advisor. Consider consulting a qualified professional before making financial decisions.

By Debt Planner Team, Content Team

Key Takeaways

- Northwestern's 2012 Kellogg study showed consumers using the debt snowball were more likely to eliminate all debt even when it was not the lowest-interest sequence.

- Fidelity states the avalanche method targeting highest rates first "generally saves you the most on interest payments, particularly if you have loans with a wide range of interest rates."

- The debt snowball, introduced by Dave Ramsey in 1997, rolls each paid-off minimum into the next-smallest balance to create behavioral momentum.

- When interest rates vary widely, the avalanche cuts total interest paid while the snowball improves completion rates according to peer-reviewed behavioral data.

In 1997, Dave Ramsey first codified what he called the 'debt snowball' inside a small Tennessee radio studio, borrowing the metaphor from a simple physics observation: a snowball rolling downhill gathers mass and momentum. At the time, behavioral economics barely existed as a field, and the idea that psychology could outperform pure mathematics in a personal finance strategy seemed absurd to most credentialed advisors. Nearly three decades later, with peer-reviewed research and AI modeling tools now available to everyday consumers, we finally have the evidence to settle the snowball-versus-avalanche debate properly.

The debt snowball method is, at its core, a sequencing decision. Research from the Kellogg School of Management at Northwestern University found that consumers who paid off their smallest balances first were more likely to eliminate their overall debt load, even when this approach was not the most mathematically efficient strategy. That finding, published in 2012, has held up against subsequent behavioral research. The debt avalanche method, by contrast, minimizes total interest paid by targeting the highest interest rate first, and Fidelity's Learning Center confirms it 'generally saves you the most on interest payments, particularly if you have loans with a wide range of interest rates.' Both statements are true. They are also in direct tension with each other, and that tension is exactly what makes this debate worth resolving with actual numbers rather than personal finance folklore.

The Core Difference Between Snowball and Avalanche

Two methods. One goal. Completely different sequencing logic.

The debt snowball lists your debts from smallest balance to largest. You make minimum payments on everything, then throw every extra dollar at the smallest balance until it's gone. When it's cleared, that payment rolls into the next smallest. The debt avalanche lists debts from highest interest rate to lowest. Same minimum-payment discipline, but extra dollars attack the most expensive debt first.

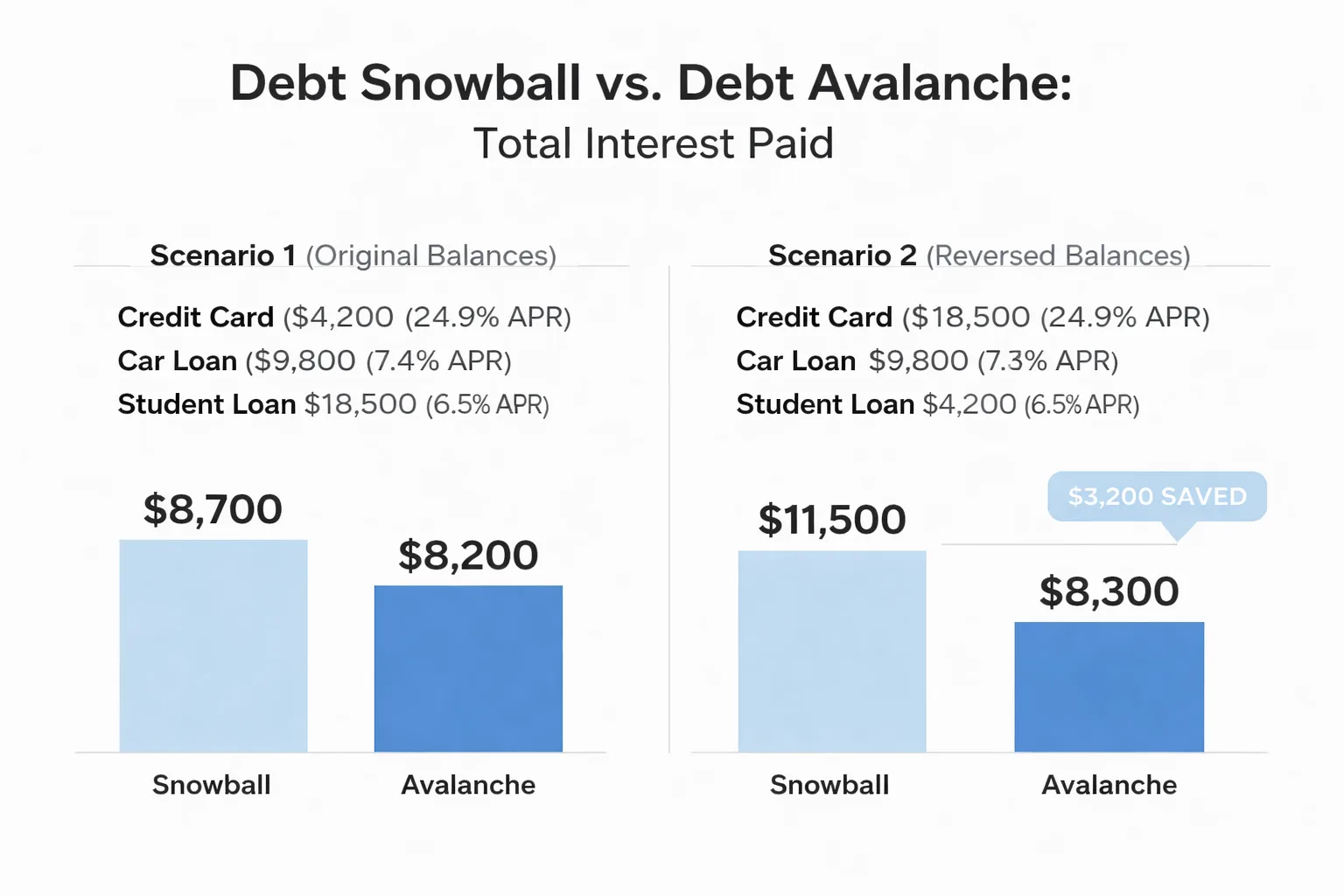

Here's a concrete 2026 example using three realistic debts:

- Credit card: $4,200 balance, 24.9% APR. Car loan: $9,800 balance, 7.4% APR. Student loan: $18,500 balance, 6.5% APR

Total debt: $32,500. Monthly extra payment available: $300.

Snowball order: Credit card first ($4,200), then car loan ($9,800), then student loan ($18,500).

Avalanche order: Credit card first (24.9%), then car loan (7.4%), then student loan (6.5%).

In this particular example, the snowball and avalanche share the same first target: the credit card. That's a coincidence of the numbers, not a rule. Change the credit card balance to $12,000 while keeping the car loan at $9,800, and the two methods immediately diverge. The snowball attacks the car loan next; the avalanche stays on the credit card. That divergence is where the interest savings (or losses) accumulate.

For a side-by-side breakdown of how these two methods play out across multiple debt scenarios, the Debt Snowball vs Avalanche vs Proportional Calculator on Free Debt Planner runs all three approaches simultaneously so you can see the gap before committing.

Which Method Saves You More Money?

Avalanche wins on interest. Full stop. The question is by how much.

Using the same three-debt example above (credit card at 24.9%, car loan at 7.4%, student loan at 6.5%), with a $300 monthly extra payment, the interest savings from choosing avalanche over snowball are real but not always dramatic when the highest-rate debt is also the smallest balance. The credit card being both the smallest balance AND the highest rate means both methods agree on the first target, compressing the savings gap.

Now stress-test the scenario. Flip the balances: credit card at $18,500 (24.9% APR), car loan at $9,800 (7.4%), student loan at $4,200 (6.5%). Same total debt, same extra $300/month. Now the methods split immediately. Snowball clears the student loan first ($4,200), then the car loan, then finally attacks the $18,500 credit card that has been compounding at nearly 25% the entire time. Avalanche goes straight at the credit card. The difference in total interest paid in this reversed scenario can reach several thousand dollars over a 4-5 year payoff horizon, because high-rate balances compound aggressively while you're busy clearing low-rate debts. That's not a rounding error. That's a vacation, a car repair fund, or months of accelerated mortgage payments.

Fidelity's guidance is explicit: the avalanche method's advantage grows specifically when your interest rates vary widely. If your rates are clustered within 3-4 percentage points of each other, the mathematical edge shrinks to the point where motivation and consistency matter more than sequencing.

One underappreciated variable: debt consolidation. If you can refinance a high-rate credit card balance into a personal loan at 12-14% APR, the avalanche's target shifts and the total interest saved by either method drops. Before committing to either strategy, it's worth understanding what debt consolidation actually does to your repayment math. Consolidation isn't always the right move, but ignoring it as an option while debating snowball versus avalanche is like arguing over which lane to drive in without noticing there's a faster road.

Why the Math Alone Doesn't Decide This

Here's the contrarian take that most personal finance writers won't say plainly: the optimal debt reduction strategy is the one you don't quit. A mathematically perfect avalanche plan abandoned after eight months beats nothing. A psychologically sustainable debt snowball completed over three years beats both.

The Kellogg School research found that the snowball method's power comes from a specific psychological mechanism: account closure. Eliminating a debt account entirely, regardless of its size, produces a measurable motivational effect. It's not just about the balance dropping. It's about the account disappearing from your list. That moment of closure triggers what behavioral economists call a "completion effect," and it's disproportionately powerful compared to what the numbers would predict.

This matters in 2026 more than it did in 2012. A CFPB survey conducted between October 2023 and January 2024 found that 61% of borrowers who received debt relief reported positive life changes, and the same survey revealed that 42% of federal student loan borrowers have only ever used the standard repayment plan, suggesting that most people default to whatever requires the least active decision-making. The implication: most people are not optimizing at all. Any structured strategy, snowball or avalanche, outperforms passive minimum payments by a wide margin.

The dropout risk is real and it's asymmetric. Avalanche plans often require months of aggressive payment before a single account closes, especially when the highest-rate debt also carries the highest balance. During that period, the debt list looks identical to where it started. For someone already anxious about their finances, that stagnation feels like failure even when the math is working perfectly. The snowball delivers a visible win faster, and visible wins are what keep people engaged long enough to finish.

For a deeper look at how debt payoff decisions interact with your credit profile over time, the credit score and debt explainer on Free Debt Planner covers how account closures, utilization changes, and payoff sequencing each affect your score, sometimes in ways that cut against the purely mathematical recommendation.

Not sure whether snowball or avalanche fits your debt profile?

Calculate My Payoff Plan →

How to Choose the Right Debt Reduction Strategy

Stop treating this as a binary choice. The real decision is a function of your specific debt profile, not a universal rule.

Run through this checklist before picking a method:

Your interest rates are within 5 percentage points of each other. If your debts are all clustered between 6% and 11%, the avalanche's mathematical edge is minimal. The snowball's motivational advantage likely outweighs the small interest difference. Go snowball.

You have one debt with a rate above 18%. This is the credit card problem. A 24.9% APR debt compounding while you clear smaller balances is genuinely expensive. If you have a high-rate debt sitting at 20%+ APR, the avalanche saves real money. Go avalanche, or consolidate the high-rate balance first and then reassess.

You have more than five separate debts. A long debt list is mentally exhausting. The snowball's account-closure mechanic is most valuable here because it shortens the list visibly and quickly. The psychological relief of going from seven debts to five, then three, is not trivial.

You've tried to pay off debt before and stopped. Past dropout is the single strongest predictor of future dropout. If you've abandoned a plan before, the snowball's quick wins are not a luxury. They're a structural safeguard against repeating the pattern.

Your largest debt is also your highest-rate debt. This is the scenario where avalanche and snowball converge naturally. Both methods target the same debt first, so the decision is moot. Pick whichever framing motivates you more.

For student loan borrowers specifically, the sequencing decision gets complicated by income-driven repayment options, potential forgiveness programs, and the fact that federal student loans carry fixed rates that are often lower than private debt. The student loan repayment strategies covered on Free Debt Planner address these variables directly, because a blanket "pay highest rate first" instruction applied to federal loans can cost borrowers forgiveness eligibility they didn't know they had.

One more variable worth naming: the emergency fund question. Aggressively paying down debt while holding no cash buffer is a plan that works until one unexpected expense destroys it. The emergency fund vs. debt payoff framework is a genuine tension, not a solved problem, and your answer to it should inform how aggressively you apply either method.

Does the Avalanche Work Better With Refinancing?

The honest answer: probably yes, but the research doesn't quantify it cleanly.

Fidelity states that the avalanche method saves more on interest, but provides no empirical case data comparing avalanche-plus-refinancing against snowball-alone. No major servicer has published a rigorous dollar-for-dollar comparison of these combined strategies. That gap in the research is worth acknowledging rather than papering over with invented numbers.

What logic and available data do support: if you can reduce the interest rate on your highest-rate debt through refinancing or consolidation before applying the avalanche method, you're compressing the rate spread that the avalanche is designed to exploit. This is not a contradiction. It means the optimal sequence is often: consolidate or refinance high-rate debt first, then apply avalanche to whatever remains. The snowball, by contrast, is largely indifferent to refinancing because it's sequencing by balance, not by rate.

For credit card debt specifically, balance transfer cards with 0% promotional APR periods can function as a temporary refinancing tool. The understanding credit card minimum payment calculations article explains why minimum payments are structured the way they are and how promotional rates interact with your actual payoff timeline, which matters enormously if you're planning to use a balance transfer as part of an avalanche strategy.

Use a Debt Payoff Calculator to Run Your Own Numbers

All of the above is framework. What actually moves the needle is seeing your specific numbers.

The Free Debt Planner debt snowball vs. avalanche comparison tool lets you enter your actual balances, interest rates, and monthly extra payment, then shows you the side-by-side projection: total interest paid, months to payoff, and the order each debt gets cleared under both methods. The gap between the two methods in your specific situation might be $200 or $4,000. You won't know until you run it.

Using a debt payoff calculator also forces a useful discipline: it requires you to list every debt, every rate, and every balance in one place. Most people who do this for the first time are surprised by the total. The act of building that list is itself a debt reduction strategy, because you can't optimize what you haven't measured.

The data from the CFPB shows that 42% of federal student loan borrowers have never moved off the standard repayment plan, which is neither snowball nor avalanche. It's passivity. Any active strategy, run consistently, produces better outcomes than the default. The calculator is the tool that turns a decision about method into a concrete payoff date on a calendar.

If you're also carrying mortgage debt and wondering whether accelerating payments fits into either framework, the dynamics are different enough that they deserve separate treatment. Mortgage acceleration involves equity, tax deductions, and opportunity cost calculations that don't apply to consumer debt. The Fed rate environment in 2026 makes this decision more nuanced than it was two years ago, and understanding how rate movements affect your debt strategy is worth doing before you redirect extra cash toward your mortgage versus your credit cards.

The bottom line on snowball versus avalanche in 2026: the avalanche wins on paper when your rate spread is wide. The debt snowball wins in practice when motivation is the binding constraint. The right answer is the one that matches your psychology to your math, and the only way to find that answer is to run your actual numbers through a tool that shows you both projections side by side.

Frequently Asked Questions

Is the debt snowball method ever mathematically better than the avalanche?

Rarely, but it can be in one edge case: when the smallest-balance debt also carries the highest interest rate. In that scenario, both methods target the same debt first, and the snowball's psychological benefits come at zero mathematical cost. Outside of that coincidence, the avalanche always pays less total interest when rates vary meaningfully.

How much extra money do I need each month to make either method work?

Both methods work with any amount above the minimum payments. Even $50/month in extra payments accelerates payoff and reduces total interest. The larger the extra payment, the more the avalanche's mathematical advantage compounds, because high-rate balances get eliminated faster before they accumulate additional interest charges.

Can I switch from snowball to avalanche mid-plan?

Yes. Many people start with snowball to build momentum, clear one or two small accounts, then switch to avalanche once they feel confident in the habit. The transition point is usually after the first account closes. The only cost of switching is a recalculation of your payoff order, which any debt payoff calculator handles automatically.

Does paying off debt with either method hurt my credit score?

Closing accounts can temporarily affect your credit utilization ratio and average account age, but the long-term effect of paying off debt is positive. The credit score timeline after paying off debt explains the specific mechanics and typical recovery windows after each account closes.

What if I have both federal student loans and high-rate credit card debt?

This is the most common real-world scenario and the one where blanket advice fails most often. Federal student loans may qualify for income-driven repayment or forgiveness programs that make aggressive payoff counterproductive. In most cases, the right move is to apply avalanche logic to private, high-rate debt while making minimum payments on federal loans and evaluating forgiveness eligibility separately.

How does inflation in 2026 affect which method to choose?

High inflation environments erode the real value of fixed-rate debt over time, which slightly favors holding fixed-rate debt longer rather than aggressively paying it down. Variable-rate debt, particularly credit cards with rates above 20%, behaves differently: the rate itself can rise with monetary policy, making aggressive payoff more urgent. In a mixed-rate debt portfolio, inflation reinforces the avalanche's logic for variable-rate balances specifically.

Enter your balances and rates into Free Debt Planner's calculator to see exactly how much each method costs you — and which one gets you debt-free first.

Calculate My Payoff Plan

Published with Meev

Important: Debt Planner is an educational tool only. We are not licensed financial advisors, credit counselors, or debt management professionals. All calculations are for educational purposes. Please consult qualified financial professionals before making significant financial decisions.

© 2025 Debt Planner. All rights reserved.